United Kingdom Rental Car Insurance- All-in-One Guide

Renting a car in the United Kingdom opens up endless opportunities to explore its rich history, scenic countryside, and bustling cities. However, before hitting the road, it’s essential to understand the ins and outs of car rental insurance in the UK. This guide covers everything you need to know to make your trip smooth, secure, and stress-free.

Renting a Car in the UK- The Essentials

To rent a car in the UK, you’ll need to prepare the following documents:

- A Valid Driver’s License: Licenses issued within the EU/EEA are accepted without additional documentation. Non-EU/EEA drivers will require an International Driving Permit (IDP). Be sure to get one before setting off.

- A Credit Card: Most rental companies require a credit card under the primary driver’s name for deposit purposes. A debit card may be accepted but will incur a higher deposit, check with the rental company first.

- Minimum Age Requirement: Most companies set the minimum age at 21, but additional fees often apply to drivers under 25 or over 70.

- Identification: A valid passport or government-issued ID is required for verification. Naturally, the name must match the one in the booking and on the credit card.

If you’re unsure about your eligibility, check the specific requirements of your chosen rental provider ahead of time.

Mandatory Rental Car Insurance in the UK

The UK’s car insurance laws require all rental cars to include Third-Party Liability Insurance. This basic coverage is a legal necessity and provides protection against:

- Injury or damages to third parties: Covers costs for accidents where you’re at fault.

- Property damage: Includes damages caused to another person’s property.

However, Third-Party Liability does not cover:

- Damage to the rental car itself.

- Theft or personal injury to the driver and passengers.

These gaps make additional insurance highly advisable for renters.

Additional Rental Car Coverage In the United Kingdom

When renting a car in the UK, you’ll encounter various optional insurances designed to reduce financial risk:

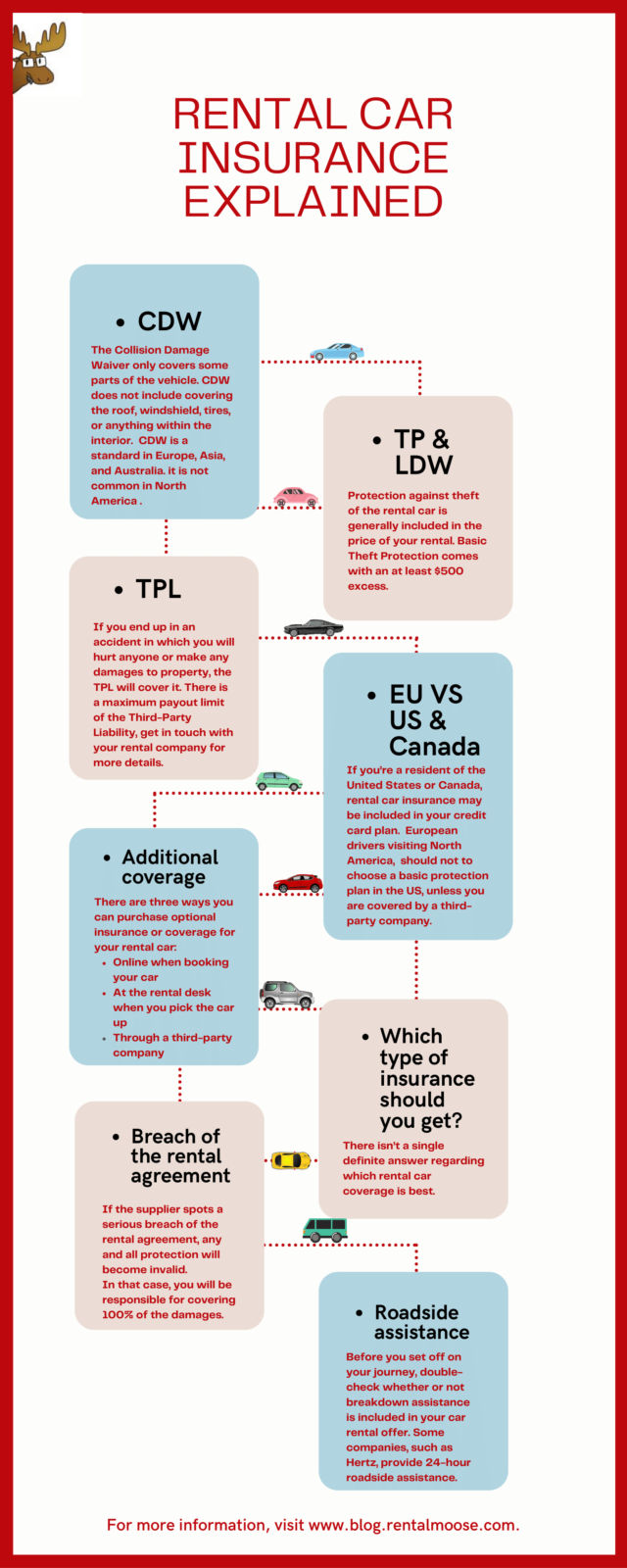

Collision Damage Waiver (CDW)

CDW limits your financial responsibility for damage to the rental car. While most UK rentals include basic CDW, it often comes with a high excess (deductible). Adding a Super CDW can further reduce or eliminate this excess, giving you peace of mind.

What CDW Covers:

- Collision-related damages.

- Repairs required due to accidents.

What CDW Does Not Cover:

- Damages to windows, tires, or the undercarriage.

- Lost or damaged keys.

Theft Protection (TP)

Theft Protection reduces liability if the rental car is stolen. While essential, it also often comes with an excess that can be reduced through additional coverage.

Key Points About TP:

- Does not cover personal belongings left in the car.

- Always ensure the vehicle is locked and parked securely.

Personal Accident Insurance (PAI)

PAI covers medical expenses for the driver and passengers in the event of an accident. However, many travelers find they already have this coverage through travel insurance.

Windscreen, Tires, and Undercarriage Protection

Standard CDW may exclude certain parts of the car, such as:

- Windscreens and windows.

- Tires.

- Undercarriage.

Adding this specific protection can save you from unexpected repair bills for these often-vulnerable components.

Glossary- Car Rental Insurance Terms to Understand

Understanding the terminology used in car rental insurance is crucial:

- Excess/Deductible: The amount you’re responsible for paying before insurance covers the rest. Higher excess usually means lower upfront costs.

- Zero-Excess Insurance: A policy that eliminates the excess entirely, albeit at a higher daily rate.

- Exclusions: Conditions or scenarios not covered by insurance, such as driving under the influence or off-road.

Reporting Rental Car Damage Claims

Should you encounter an accident or damage the vehicle, follow these steps:

- Document the Scene: Take photos of any damage and note the time and location.

- Notify the Rental Company: Report the incident immediately to avoid complications.

- Complete an Accident Report Form: Most rental providers will require this document for insurance claims.

- Understand Your Liability: Review your coverage to know what costs you may be responsible for.

Bonus- Navigating Tolls and Congestion Zones

The UK has a network of toll roads and congestion charges, particularly in London. Most rental providers offer solutions such as automatic toll devices or advice on paying charges. Ensure you understand:

- Congestion Charge Zones: Check if your route includes restricted areas like central London.

- Toll Roads: Examples include the M6 Toll in the Midlands.

Failing to pay these fees can result in fines, which are often passed onto the renter with additional admin charges.

Why Choose Rentalmoose for Your UK Road Trip

Booking your rental car with Rentalmoose ensures a seamless and reliable experience. Say goodbye to hidden fees and unexpected costs. Rentalmoose plants a tree for every booking!